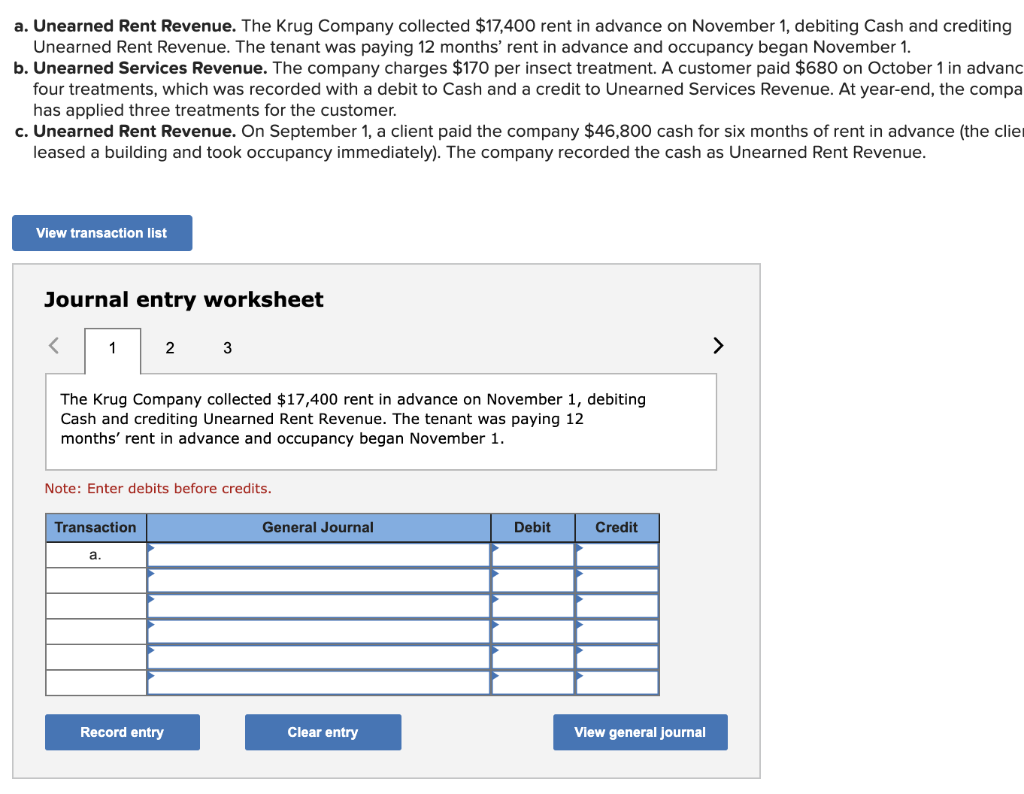

Purchasing property isn’t any brief decision, however when it comes to strengthening property, this new stakes was even higher. Anywhere between finding the right hiring business, fulfilling strengthening requirements and you will finding out their mortgage repayments, building your residence can end up being a frightening task. A construction loan essentially a sum of money you are free to financing your own building will cost you helps you manage the newest financial regions of this performing.

What’s a construction Loan?

![]()

After you purchase a home, your safer an interest rate. But when you create property, you will likely have to take out a more certain form of out-of mortgage called a construction financing. As they are experienced a monetary risk with the bank, they often provides higher interest rates.

To possess structure loans, the financial institution pays the building specialist actually in the place of providing the currency to your citizen https://paydayloanalabama.com/penton/. Such payments can be found in periodic stages over the course of the latest building processes. They come always due to the fact builders enjoys met specific observable standards. Since developers have finished our home, this new homeowner commonly typically have reduced the mortgage in full. If you don’t, the borrowed funds might be transformed into a permanent home loan towards a portion of the debtor.

The many Kind of Structure Funds

Just like with typical mortgage loans, you to definitely size will not fit all of the which have framework loans. Here good around three chief brand of constructions funds you can also run into:

- Construction-to-permanent fund

- Stand-alone design fund

- Repair structure fund

Inside the a casing-to-permanent loan (often referred to as a single-intimate financing), your borrow cash to help you pay for the development off the house by itself. When you transfer to your brand new domestic, the mortgage immediately becomes a home loan. At the time of your own closure, you will cement your rate of interest. For those with firm arrangements for their home’s build, an individual-personal mortgage will give an equally firm set rate of interest that was unlikely so you can change.

The next main type, stand-alone (also called two-close) construction finance, are usually a couple separate loans. Essentially, your first financing covers the building. When you complete the home and tend to be set to move around in, you will get a home loan. You to definitely next financing is always to pay the debt you incurred out of design. Stand-alone design money try best for you when you have large cash on give. Same thing if you aren’t set in a relationship which have a lending lender by the time strengthening kicks off.

The 3rd head form of construction financing is named a restoration framework mortgage. With a remodelling construction mortgage off a dependable lender, anyone can get prepare the expenses of whole build and restoration toward final mortgage. The fresh new projected property value the house just after fixes and you may home improvements will determine the dimensions of the mortgage. These are mainly for those looking to purchase a home from inside the demand for big fixes. We frequently relate to these home while the fixer-uppers.

Exactly what do Framework Funds Shelter?

Structure finance might be of great assistance to any individuals otherwise parents seeking create the place to find their hopes and dreams, in place of to shop for an existing design. However, a homes financing discusses several additional house-purchasing efforts.

Especially, which list has the purchase price of the block of land on what you should build your family and the cost out-of closure the offer. As well, of many loan providers should include a condition taking currency to have very-calledsmooth can cost you particularly house package structure charges, physical technologies and you can work and you may property it allows.

Build finance safeguards a vast assortment of will set you back. They’re able to connect with several house purchase and you may revamp need, and focus on first-go out household builders. Thus, they are an attractive choice for your investment.

Area of the differences when considering the types of build loans spring away from perhaps the debtor is building another type of family or remodeling an earlier that. Regarding a separate build, their financial would like to make sure to are located in a solid place economically and that you features real and you may possible arrangements for your home.

When your financial takes into account you a viable applicant, they will give the development loan. You get the bucks from inside the occasional installment payments since your house’s building processes requires function. Whenever you are more likely in order to spruce up a great fixer-higher, the loan will alternatively getting factored to your permanent mortgage.

Bottom line

Put simply, construction money performs by permitting basic-go out home designers which have sufficient fico scores to execute its enterprise arrangements. As usual, the connection between the lender while the borrower was keymunication towards the the new area of the bank, the new debtor and also the creator are required.

Just like any financing, thought cautiously the new terms of the borrowed funds as well as influence on your bank account. Also, it is smart to work on a financial advisor observe how it matches in the financial plan.